As borrowers prepare to resume student loan repayment after nearly five years of payment pauses and extensions, some people may be looking to save money on interest through student loan refinancing.

Why It Matters

Student loan borrowers have struggled to keep up with payments, even before the federal payment pauses that came as part of the CARES Act in 2020. Findings from the Education Data Initiative show that over 10 percent of borrowers default in their first three years of payment on their student loans.

As of January 2024, about 30 percent of borrowers were past due on payments. Accumulating interest has been a barrier to borrowers paying off their loans and refinancing is one option to get a lower interest rate and decrease the amount that builds up over time.

What To Know

Federal student loan forbearance, or the temporary pause on loan payments, began for borrowers in March 2020 in response to the COVID-19 pandemic and ended in August 2023.

Millions of borrowers were past due on their payments as of January 2024, according to the U.S. Government Accountability Office, and one in four borrowers said they were struggling to pay their bills in a June Bankrate survey.

Student loan refinancing could be a strategic move for borrowers looking to save money on student loan interest payments, as refinancing often means taking out a new loan with a lower interest rate to pay off an existing loan with a higher rate. A major factor to consider when weighing the option of refinancing is the type of student loan: private vs. federal.

While some private loan lenders only have fixed APRs, or rates that don't change, others have variable APRs, which do change. Many lenders offer loans with both types of interest.

Why You Should Refinance a Student Loan

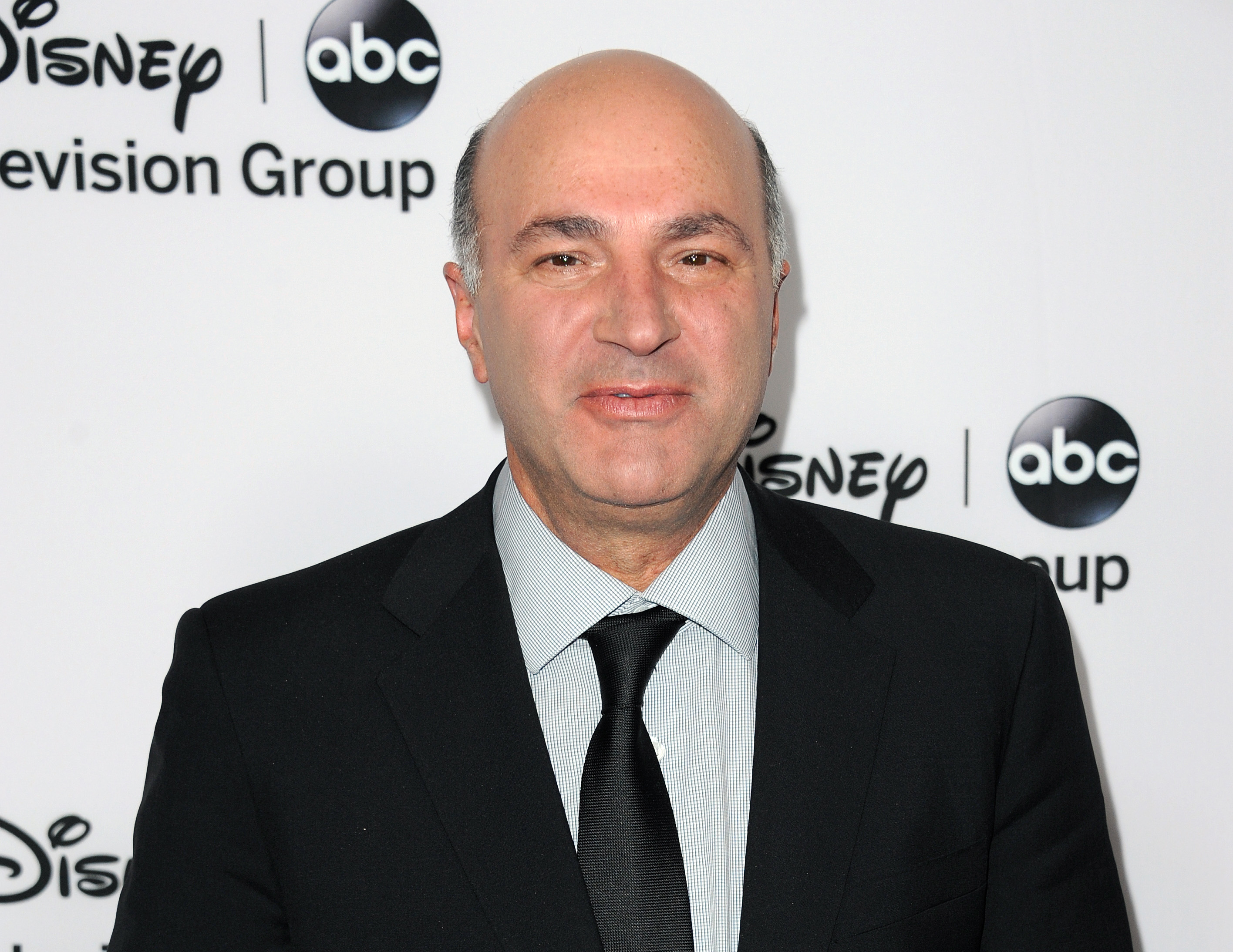

If a person has a variable interest rate, they could secure a lower rate through refinance, which could result in "substantial savings," Kevin Thompson, finance expert and founder/CEO of 9i Capital Group, told Newsweek.

Further, if rates have dropped since a person got their variable interest loan, refinancing could give them the opportunity to get on a fixed-rate loan and have more stability.

Alex Beene, financial literacy instructor for the University of Tennessee at Martin, told Newsweek the "smart rule" is usually to only refinance a student loan if you can receive a lower interest rate.

"If the student debt holder is having to pay back a private loan with a high interest rate, refinancing to a lower rate can lead to less interest paid over time and a smaller monthly payment," Beene said.

Why You Shouldn't Refinance a Student Loan

Michael Lux, an attorney and founder of Student Loan Sherpa, told Newsweek it's not usually smart for people with federal student loans to refinance them.

Borrowers who have a SAVE repayment plan are currently on interest-free forbearance while the legality of the plan is litigated in court. Lux noted that a refinance lender isn't going to give borrowers a 0 percent interest rate, so they're better off waiting to see what happens with court rulings. And, if you refinance a federal loan, borrowers lose their protections.

"With federal loans, borrowers should proceed with extreme caution. Once you refinance a federal loan, you permanently erase important borrower protections like income-driven repayment and student loan forgiveness." Lux said.

What People Are Saying

Kevin Thompson, finance expert and founder/CEO of 9i Capital Group, told Newsweek: "If refinancing isn't the right option, focusing on paying off privately funded loans first could be more effective, as they often have fewer flexible repayment options. Using the avalanche method to target loans with the highest interest rates can save the most money over time. Alternatively, if you prefer to focus on psychological wins, paying off loans with the highest balances may help you feel more accomplished as you reduce your overall debt."

Alex Beene, financial literacy instructor for the University of Tennessee at Martin, told Newsweek: "Sadly, too many focus on just lowering their monthly student loan payment. Yes, in the short term, it's great to owe less each month and free up cash for other expenses. However, in the long term, that debt is sticking around. Your ultimate goal is to pay that debt off. Refinancing is a step to lower the burden interest plays in that process, and if used as such, it can save you substantial money over time."

What Happens Next

Whether or not you decide to refinance your student loans will likely depend on your personal financial needs. Be sure to contact your loan servicer to understand your options with regard to refinancing.

Federal student loan forbearance, or the temporary pause on loan payments, began for borrowers in March 2020 in response to the COVID-19 pandemic. This forbearance officially ended in August 2023, but borrowers who applied for the SAVE plan were placed on an interest-free general forbearance while the legality of the SAVE plan was challenged in court. Those borrowers still remain in this forbearance.

English (US) ·

English (US) ·